By Christopher Combs, AI Assisted

Chief Investment Officer

Silicon Valley Capital Partners

Executive Summary

Artificial intelligence is now exerting measurable influence on the U.S. labor market, enterprise spending patterns, and monetary policy. The latest MIT “Iceberg Index” confirms that 11.7% of American jobs are already exposed to tasks that current AI systems can perform, representing $1.2 trillion in annual wages tied to functions ripe for automation or augmentation.

The enterprise adoption curve is also taking shape. Global companies are currently in the earliest stage of the AI investment cycle — the “operational lift-off” phase, where only 11–15% of firms have begun deploying AI at scale. This moment is comparable to the early innings of cloud computing in 2007–2010, when early adopters quietly began building permanent advantages.

From here, enterprise AI spend will accelerate sharply:

- Within 5 years: adoption rises to 40–50% of global enterprises

- Within 10 years: AI reaches 80–90% penetration, becoming standard operational infrastructure

- Total cycle length: 10–12 years, with peak capex intensity during years 4–8, as companies rebuild data pipelines, deploy private models, and integrate AI copilots into core systems

These structural developments will also influence monetary policy. As AI reduces wage pressure through productivity gains and task-level automation, the labor market becomes less inflationary, likely prompting a more dovish Federal Reserve over the next several years.

The strategic choice facing enterprises is clear: invest early and build compounding productivity advantages, or fall behind competitors who harness AI to operate faster, leaner, and smarter.

AI Implementation Is Significant and Will Force a Stand-Up Across Global Enterprises — Those Who Don’t Invest Will Fall Behind

Artificial intelligence has crossed a decisive threshold. It has moved from an experimental technology to an economic force reshaping job design, wage structures, enterprise costs, and competitive strategy. This is not a cyclical change — it is a structural shift that will influence corporate operating models for decades.

The recent MIT Iceberg Index offers one of the clearest data signals to date. By modeling task-level exposure across 151 million U.S. workers, MIT found that 11.7% of the labor market is already reachable by today’s AI systems. The affected roles are not centered in Silicon Valley or technical fields—they are embedded in the administrative, clerical, and operational backbone of American business.

This dispersion, across industries and geographies, elevates AI from “innovation initiative” to a mandatory strategic priority.

- AI’s Economic Impact Is Wider Than Expected — A Task-Level Transformation

Contrary to common perception, the highest exposure to AI is not among programmers or data scientists. MIT’s data shows the deepest impact occurs in the routine, document-heavy functions that exist everywhere:

Operational categories with the highest AI exposure

- Document processing: claims, invoice matching, financial close, compliance

- Clerical support: HR workflows, payroll routing, timekeeping systems

- Back-office operations: procurement, logistics coordination, scheduling

- Structured customer support: call centers, underwriting intake, fielding tier-one issues

These categories contain thousands of small, repetitive tasks, many of which are rules-based and deterministic — making them ideal candidates for LLMs, agentic systems, and process automation.

Why AI changes the cost structure

AI doesn’t need to replace entire jobs; it merely needs to automate 20–50% of a workflow to materially change the economics of labor. Companies that automate portions of high-volume workflows immediately:

- Reduce labor hours per process

- Improve accuracy and reduce error propagation

- Accelerate cycle times

- Lower per-unit cost

- Reallocate labor toward higher-value functions

As a result, AI’s economic footprint is expanding horizontally across sectors, touching everything from insurance to healthcare to state government operations.

Conclusion:

The AI transition is primarily a task-level revolution, not a job-level collapse — and it is already altering the economics of core business operations.

- Governments Are Now Adjusting Workforce Infrastructure — A Multi-Year Re-Training Cycle

Multiple U.S. states have begun translating AI exposure into policy action. Tennessee, North Carolina, and Utah are among the earliest adopters, using Iceberg Index data to restructure workforce planning.

Technical design components of these programs

-

-

- Statewide AI exposure heat maps

Identifying the counties and job categories most at risk. - Targeted retraining curricula

Community colleges shift toward digital operations, data handling, and AI-assisted workflows. - Automation pilots within state agencies

Early use cases include benefits processing, licensing workflows, and public-records routing. - AI model evaluation boards

Agencies establish standards for bias measurement, privacy safeguards, model provenance, and auditability. - Workforce transition frameworks

Helping workers pivot from legacy clerical roles into higher-demand digital operations roles.

- Statewide AI exposure heat maps

-

The scale and structure of these programs indicate that AI’s labor-market impact is now recognized as structural rather than cyclical.

Conclusion:

Government retraining infrastructure is now underway — an early signal of how nations will adapt to AI-driven labor realignment.

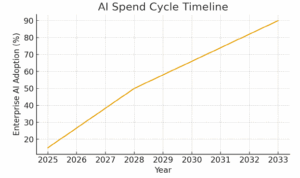

- The Enterprise AI Spending Cycle Has Entered “Operational Lift-Off” — With a Decade of Growth Ahead

Each major technological era follows a multiyear capex cycle. AI is now entering the beginning of its own.

Where enterprises are today

Only 11–15% of global corporations are deploying AI operationally — training private models, implementing copilots, modernizing data pipelines, or deploying AI agents for workflows.

The next stages of the cycle

Stage 1: Operational Lift-Off (Year 0–3, now underway)

- Private model pilots

- Standalone AI tool adoption

- Initial workflow automation

- GPU and inference infrastructure investment

Stage 2: Accelerated Adoption (Year 3–8)

- AI copilots embedded into enterprise software

- AI-native ERP and HRIS systems

- Complete data architecture modernization

- Broad departmental automation

- Peak capital expenditures

Stage 3: AI-Native Infrastructure Standardization (Year 8–12)

- AI integrated across all core operations

- Industry-specific AI models

- Competitive pressure forcing universal deployment

- AI cost savings recycled into new tech initiatives

Why early adopters win long-term

Because AI generates compounding productivity, early movers lock in:

- Lower operating costs

- Faster decision cycles

- Higher output per worker

- Better forecasting and planning accuracy

- Superior customer experience

- Wider margins across economic cycles

These advantages become difficult and expensive for late adopters to overcome.

Conclusion:

The AI investment cycle will run 10–12 years, with broad adoption by 80–90% of global enterprises by the end of the decade.

- AI Will Influence Federal Reserve Policy — Creating a More Dovish Bias

The Federal Reserve’s employment mandate will increasingly intersect with AI-driven labor dynamics. Because AI modifies how labor markets tighten, loosen, and inflate, the Fed will be forced to incorporate AI into its long-term framework.

AI influences the Fed through four channels

- Job turnover and reallocation

AI increases transitions without increasing unemployment, creating softer labor tightening. - Reduced wage inflation at the clerical layer

As AI automates administrative tasks, wage pressure in these categories moderates. - Productivity-driven disinflation

Output rises faster than labor input, lowering unit labor costs. - Regional shifts untethered from recessions

AI exposure may cause local labor softening even in economic expansions.

The policy implication

As AI reduces wage-driven inflation pressures, the Fed gains additional room to ease without destabilizing price stability. Over the next several years, this dynamic is likely to produce:

- A more accommodative rate path than markets expect

- Earlier rate cuts during future slowdowns

- Lower perceived terminal rates

- A gradual downward pull on long-term neutral rate estimates

Conclusion:

AI becomes a structural force pushing the Federal Reserve toward a dovish tilt — a shift not yet fully reflected in market pricing.

Final Perspective

AI has moved from the periphery of corporate planning to the center of economic and labor-market strategy. It now influences job design, wage patterns, enterprise spending, government policy, and central-bank decision-making.

The strategic takeaway for corporate leaders is straightforward:

- Stand up, experiment, and invest early, building durable, compounding productivity advantages

or - Fall behind competitors who adopt AI-native operating models and operate leaner, faster, and more efficiently

In every technological revolution of the past century, early adopters captured the lion’s share of efficiency gains and market share. The AI era will be no different — but the gap will widen faster than any prior cycle.